Submitted by Dallas Kachan on

It’s December again (how did that happen!?) and our annual time for reflection here at Kachan & Co. So as we close out 2011, let’s look towards what the new year may have in store for cleantech.

There are eggshells across the sector for 2012. Global economic uncertainty in particular is leaving some skeptical about the chances for emerging clean technologies. And those who watch quarterly investment data, or who look only in a single geography (e.g. North America) may have seen troubling trends brewing this past year. But the true story, and the global outlook for the year ahead, is—as it always is—more complicated.

As you’ll read below, we predict a decline in worldwide cleantech venture capital investing in 2012. But as you’ll also read below, we believe the gap will be more than made up by infusions of corporate capital. And the exit environment, depending on who you are and where you list, still looks robust in 2012 for cleantech (it may not have felt so, but it was actually surprisingly robust in 2011, according to the data. See below.) All in all, if you’re a cleantech entrepreneur seeking capital, our advice is brush up that PowerPoint and work the system now… while there’s still a system to work.

Because, as we detail below, the largest risk, to cleantech and every sector in 2012 we believe, is the specter of precipitous global economic decline and the systemic changes it might bring. Details below.

Here are our predictions for cleantech in 2012:

Cleantech venture investment to decline

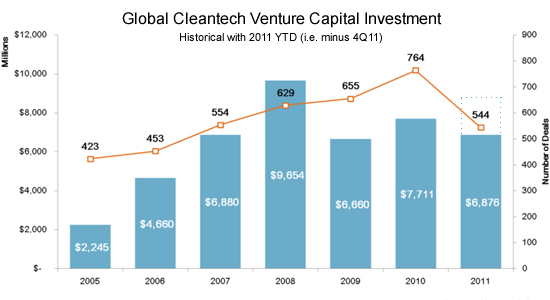

In the face of naysayers then forecasting a cleantech collapse, in our predictions this time last year, we called an increase in global cleantech venture investment in 2011. We were right. At this writing, total investment for the first three quarters of 2011 is already $6.876 billion, with the fourth quarter to report early in 2012. Given historical patterns (fourth quarters are almost always down from third quarters), we expect 2011 to close out at a total of ~$8.8 billion in venture capital invested into cleantech globally. That’d be the highest total in three years, and second only to the highest year on record: 2008.

Total 2011 investment is expected to show growth from 2010’s figures once the fourth quarter (dashed lines, estimated) is added. However Kachan predicts total venture investment in 2012 to decline from 2011’s total. Data: Cleantech Group

Total 2011 investment is expected to show growth from 2010’s figures once the fourth quarter (dashed lines, estimated) is added. However Kachan predicts total venture investment in 2012 to decline from 2011’s total. Data: Cleantech Group

Yet in 2012, we expect global venture investment into cleantech to fall. Not dramatically. But we expect cleantech venture as measured by the data providers (i.e. companies like Dow Jones VentureSource, Bloomberg New Energy Finance, PwC/NVCA MoneyTree, and Cleantech Group) to show its first decline in 2012 following the recovery from the financial crash of 2008. Our reasoning? There are factors we expect will continue to contribute to the health of the cleantech sector, but they feel outweighed by factors that concern us. Both sets below:

On one hand: What we expect to contribute to growth in cleantech investment in 2012

- China gets a hold on its economic turbulence - For five years now in our annual predictions, both here at Kachan and when I was a managing director of the Cleantech Group, we foretold the rise of China as cleantech juggernaut. Yet, now with China having become the largest market for and leading vendor of cleantech products and services by all metrics that matter, and now receiving a larger percentage of global cleantech venture capital than at any point in history, there have been recent warning signs. New data just in (for instance, falling Chinese property prices and sluggish export growth because of faltering first world economies, not to mention the first decline in clean energy project financing in China since 2010 as wind project financing declined 14% in the third quarter of 2011 on fears of over-expansion) suggests the Chinese economic engine is slowing. On the face of it, that might look bad for cleantech. But we put a lot of faith in China’s central government and the seriousness with which it views this sector as strategic. Even now, the country has just gone on the record forecasting creating 9 million new green jobs in the next 5 years. Nine million! And China has a good track record in executing its 5-year plans.

- Rise in oil prices - Cleantech is a much wider category than energy. But for many, renewable energy is its cornerstone. And while there’s no question about the long-term markets for renewables, the biggest factor affecting their short-term commercial viability is the price of fossil-based energy. The good news: indications are that oil prices are headed upwards in 2012, which should be expected to help make renewables more economic. Naysayers maintain that a poor global economy will destroy demand for energy, keeping the price of oil artificially low. For much of 2011, the price of oil was relatively low. But we argue the price per barrel will continue its inexorable rise in 2012 given continued growth in the size of the global market for oil, driven by market expansion in the developing world. Further adding to the expected oil price increase is a little-known fact: there’s been a decline in the quality of oil the world is seeing on average. And the poorer the quality of the oil, the more it costs to refine it into the products we require. Oil prices are headed up.

- Corporations’ even stronger leadership role – Corporate venturing was up in 2011, possibly setting new record highs, according to the data providers (4Q data not in yet.) Cleantech corporate mergers and acquisitions globally were up in 2011, again possibly setting new record highs, according to the data. The world’s largest companies assumed the leadership we and others predicted they would last year at this time—and indications are they will continue to do so in 2012, with balance sheets still strong.

- Solar innovation as a perennial driver - Investment into good old solar innovation and projects is still strong, and has remained so for years, while other clean technologies have risen and fallen in and out of investment fashion. And that’s despite most solar companies being in the red and having billions of dollars in market capitalization disappear over the last year. As some solar companies will continue to close up shop in 2012, look for investment into solar innovation to remain strong in 2012 as the quest for lower costs and higher efficiencies continues.

- Persistence of the fundamental drivers of cleantech - The sheer sizes of the addressable markets many cleantech companies target, and the possibilities for massive associated returns, will continue to draw investors to the sector. Why? The world is still running out of the raw materials it needs. Some countries value their energy independence. More than ever, economies need to do more with less. Oh, and there’s that climate thing.

On the other hand: What worries us about the prospects for growth in cleantech investment in 2012

- Investor fundraising climate tightening – Today, limited partners (i.e. “LPs” – the organizations and/or wealthy individuals that fund venture capital companies) are still bankrolling cleantech worldwide; in its 3Q 2011 Investment Monitor for clients, the Cleantech Group details 34 dedicated cleantech and sustainability-focused funds receiving billions in capital commitments internationally in the third quarter of 2011 alone. But we expect a slowdown in venture fundraising in 2012. Blame Solyndra for negative American LP sentiment. Or blame the lack of rock star returns in cleantech of late. But there are more indications than ever that some LPs are becoming increasingly reluctant to fund cleantech. They’ve been grousing about cleantech for years. But the politicizing of the Solyndra bankruptcy has amped the rhetoric higher than ever, and will foster a self-fulfilling prophesy in 2012, particularly in America, we believe.

- Waning policy support in the developed world – Expected conflicting government policy signals to continue in 2012. Don’t expect cleantech-friendly U.S. policy leadership in 2012, an election year. We wouldn’t be surprised if the ghost of Solyndra and other U.S. Department of Energy stimulus grants and loan guarantees continued to haunt American cleantech through the whole of 2012, making any overt U.S. government support of clean or green industry unlikely. While cleantech is far from solely an American phenomenon, there’s no mistaking that the (now expired) American national loan guarantee program helped loosen private cleantech capital in an immediately post-2008 shell-shocked economy. However, continued uncertainty over the future of the U.S. Treasury grants program and production tax credits is holding the U.S. back. Policy support suffers elsewhere in the developed world. For instance, in the UK, investor confidence was recently dealt a blow by a dramatic drop in solar feed-in-tariff (FIT) rates, and the erosion of renewable policy support in Germany and Spain is well known.

- Lag time of negative sentiment – Even if the sky indeed started falling in cleantech (and we don’t believe it yet has), it would take a few quarters to show in venture or project investment numbers. Remember, deals can take quarters to consummate. Transactions being counted now may have been initiated a year ago. Fear takes several quarters to manifest. Which is why we believe today’s uncertainty will start to show in 2012’s performance.

- VCs still circling their wagons – In 2007, before the financial crash, the percentage of early stage venture investments into new cleantech companies was roughly the same as later-stage venture investments into established companies. Since the crash of 2008, deals have remained skewed—both by number and size of deals—towards later stage companies, illustrating investors’ preference to keep existing investments alive than take risks on new companies. While the exact ratio varies quarter to quarter, and from data provider to data provider, there have been generally fewer early stage companies getting funded. That’s hampering cleantech innovation. We expect the trend to continue into 2012.

- Perennial concern about exits and IRR – Despite the size of its massive addressable markets and near-record amounts of capital entering the space today, on the whole, cleantech investors are still seeking the returns that many of their web and social media tech brethren enjoy. Even now, 10 years into this theme that we started calling cleantech in 2002. That’s not for lack of exits; 2010 saw the largest number of cleantech IPOs on record (93 companies raised a combined $16.3 billion) and 2011 has already had 35 without the last quarter reporting. And cleantech M&A activity in 2011 was strong and significantly higher than last year. No, the concern is for lack of multiples. For instance, 8 of the 14 IPOs of the third quarter of 2011 were trading below their offering price as of the publication of the Cleantech Group’s 3Q 2011 Investment Monitor. Don’t let anyone tell you exits aren’t happening in cleantech. They’re just underwhelming. And/or they’re happening in China.

- Macro-economic turbulence, collapse, or at least, reform – They’re the elephants in the room: The Occupy movement. Arab Spring. Peak Oil. The continued and growing mismatch between overall global energy supply and demand and food supply and demand. Ever-increasing debt and trade deficits. Currency revaluation or political/military developments. Any or all of these could spur another massive global economic "stair-step" downwards of the scale we saw in 2008, or worse. Concern about all of these points and the impact they’d have on the cleantech sector weighs heavy on us here.

Venture dip made up for by rise in corporate involvement

The world’s largest corporations woke up to opportunities in cleantech in 2011, making for record levels of M&A, corporate venturing and strategic investments. General Electric bought lighting and smart grid companies. Schneider Electric bought some 10 companies across the cleantech spectrum. Corporate venturing activity was high, as were minority-stake investments. In just the third quarter alone, ZF Friedrichshafen invested $187 million in wind turbine gearbox and component maker Hansen Transmissions of Belgium, Stemcor invested $137 million into waste company CMA in Australia, and BP invested $71 million into biofuel company Tropical BioEnergia in Brazil. And there were dozens more minority stake transactions like these throughout the year.

Look for even more cash-laden companies to continue to buy their way into clean technology markets in 2012, supplementing the role of traditional private equity and evidencing a maturation of the cleantech sector.

Storage investment to retreat

Significant capital has gone into energy storage in recent quarters. In 3Q11, storage received $514 million in 19 venture deals worldwide, more than any other cleantech category. Will storage remain a leading cleantech investment theme in 2012? We’re betting no. Here’s why.

Storage recently made headlines as the subsector that received the most global cleantech venture investment in the third quarter of 2011, the last quarter for which numbers are available. An analysis of the numbers, however, shows the quarter was artificially inflated by large investments into stationary fuel cell makers Bloom Energy and ClearEdge Power. Do we at Kachan expect more investments of that magnitude into competing companies? No. Why? Even if you believe analysts that assert that stationary fuel cells for combined heat and power are actually ramping up to serious volumes (oldtimers have seen this market perpetually five years away for 15 years, now), just look how crowded the space currently is. Bloom and ClearEdge are competing with UTC Power, FuelCell Energy, Altergy, Relion, Idatech, Panasonic, Ceramic Fuel Cells and Ceres Power … just some of the better-known 60 or so companies vying for this tiny market today. And many are still selling at zero or negative gross margins.

But the main reason we’re not bullish on storage: Smoothing the intermittency of renewable solar and wind power might turn out to be less important soon. Sure, nary a week goes by without announcements of promising new storage tech breakthroughs or new public support for grid storage (e.g. see these three latest grid storage projects just announced in the U.S., detailed halfway down the page.) But we believe that utility-scale renewable power storage might be obviated if utilities embrace other ways to generate clean baseload power.

In 2012 or soon thereafter, we expect those clean baseload options will start to include new safer forms of nuclear power (don’t believe us? Read Kachan’s report Emerging Nuclear Innovations—U.S. readers, don’t worry: nuclear innovation won’t apply to you.) Or NCSS/IGCC turbines powered by renewable natural gas delivered through today’s gas distribution pipelines (see The Bio Natural Gas Opportunity). Or even geothermal (gasp!) or marine power (see below). All of these promise to be less expensive than solar and wind when you factor in the expense of storage systems required—incl. electrochemical, compressed air, hydrogen, flywheel, pumped water, thermal, vehicle-to-grid or other—if solar and wind are to be relied on 24/7.

Marine energy to begin coming of age

I’m a closet fan of marine energy, despite today’s extraordinarily high cost per kilowatt hour. We started covering wave, tidal and ocean thermal energy conversion equipment makers in 2006. Anyone who’s heard me talk publicly on the subject has had to suffer through hearing how I’d much prefer invisible kit beneath the waves than have to gaze upon solar and wind farms taking land out of commission.

In 2006, the lifetime of equipment from then-noteworthy companies like Verdant Power and Finavera (which since exited marine power after a failed test with California’s PG&E) in the harsh marine environment could sometimes be measured in days. The designs just didn’t hold up. Even Ocean Power Delivery, now Pelamis Wave Power, with its huge, snakelike Pelamis device, had hiccups in early onshore grid testing. Back then, the industry clearly had a long way to go.

Today, six years later, we think it’s time to start taking marine energy seriously. A high profile tidal project is now underway in Eastern Canada’s Bay of Fundy. Several weeks ago, Siemens raised its stake in UK-based tidal energy developer Marine Current Turbines from less than 10% to 45%, because it liked the predictability of ocean energy, and Voith Hydro Wavegen handed over its first commercial wave project to Spain. And last week, Dutch company Bluewater Energy became the latest vendor to secure a demo berth at the European Marine Energy Centre at Orkney, Scotland—the most important global R&D center for marine energy. Things are going on in marine power. Still, its major hurdle is the large variation in designs and absence of consensus on what prevailing technologies will look like.

2012 won’t be the year marine power becomes cost-competitive with coal, or even nearly. But you’ll hear more about marine power in 2012, and see more private and corporate funding, we predict.

Increased water and agricultural sector activity

Look for increased venture investment, M&A and public exits in water and agriculture in 2012.

At one point, only cleantech industry insiders championed water tech as an investment category (and, frankly, at only a few hundred million dollars per year on average, it still remains only a small percentage of the overall average $7B annual cleantech venture investment.) Industrial wastewater is driving growth in today’s water investment, with two of the top three VC deals of the last quarter for which data is available promoting solutions for produced water from the oil and gas industry, and the largest M&A deal also focused on an oil and gas water solution. Regulations aimed at making hydraulic fracturing less environmentally disruptive to will spur continued innovation and related water investments in 2012.

Where water was a few years ago, agriculture investment appears to be today. There was more chatter on agricultural investment than ever before at cleantech conferences I attended around the world this past year. Expect it to reach a higher pitch in 2012, because of:

- Growing awareness of the complex interrelationship between water, energy and food

- Increased awareness of the math underlying the planet’s current population growth rate and how that’s going to impact our ability to feed the world, and

- Our reliance on inexpensive oil and gas, petroleum-based fertilizers and hybrid seeds for today’s crop yields

Investing in farmland is even resurfacing, in these uncertain times, as a private equity theme.

Remember the food crisis three years ago, when sharply rising food prices in 2006 and 2007, because of rising oil prices, led to panics and stockpiling in early 2008? Brazil and India stopped exporting rice. Riots broke out from Burkina Faso to Somalia. U.S. President George W. Bush asked the American Congress to approve $770 million for international food aid. Those days could return, and they represent opportunity for micro-irrigation, sustainable fertilizer and other water and agriculture innovation.

And so concludes our predictions for 2012. What do you agree with? What do you disagree with? Leave a comment below.

A former managing director of the Cleantech Group, Dallas Kachan is now managing partner of Kachan & Co., a cleantech research and advisory firm that does business worldwide from San Francisco, Toronto and Vancouver. The company publishes research on clean technology companies and future trends, offers consulting services to large corporations, governments and cleantech vendors, and connects cleantech companies with investors through its Hello Cleantech™ and Northern Cleantech Showcase™ programs. Kachan staff have been covering, publishing about and helping propel clean technology since 2006. Details at www.kachan.com.

Comments

I agree with you on marine energy!

Permalink Submitted by Kevin Eber (not verified) on Fri, 12/02/2011 - 09:33.

Dallas--

I agree with your take on marine energy. Like you, I'm a bit of a closet fan. As the former editor of DOE's clean energy newsletter, the EERE Network News, I covered marine energy whenever I could. My first article on the subject, published in late 2000, was about a 500-kW oscillating water column built on the Scottish island of Islay (did that one survive?). For a while there, I reported on sinkings as often as successes, but I think the industry is finally maturing. The industry has huge potential, and I can't wait to see it take off.

By the way, I'm pretty much the only reason that DOE's Energy Efficiency and Renewable Energy (EERE) Web site has included information on ocean energy pretty much since it was launched, way back in the dark ages of the Internet (when we were still using Mosaic as a browser). Even though DOE didn't have a Water Power Program back then, I insisted that we include all the RE technologies, even the ones we weren't investigating. Over the years, a lot of other institutions drew on our website when looking for ocean energy facts. So, I like to think that I did my part to help the industry along.

Oh, and I think you should add one more elephant to your room: global warming. Another big wild-card for our energy future ... and our future in general.

--Kevin Eber, NREL

Great summary. What about....

Permalink Submitted by Marc McArthur (not verified) on Thu, 12/08/2011 - 10:53.

Dallas, this was very well written and researched and an enjoyable read. Congratulations! A few of my favourite topics didn't make it to the predictions for 2012 and I hope to solicit some comments on them here. They are:

- The increasing role of buildings as the battleground for tackling energy and other resource consumption

- The Information and Communications Technologies (ICT) sector and the potential it has to be both part of the problem (inefficient data centres, end of life issues etc.) as well as part of the solution (behaviour modification, control systems etc.)

- Energy from waste and residual materials (MSW, agricultural and forestry residue)

Looking forward to your (or anyone else's) thoughts on what these areas will be like in cleantech over the coming year.

What about fusion power

Permalink Submitted by Ron (not verified) on Thu, 12/08/2011 - 11:52.

I read a blogger's description of your report in fusion power, including reference to a highly discrete Australian entrepeneurial group you interviewed who say that after over a decade of quiet research they will be bringing out a fusion powered energy device in 2012. I was hoping you might be sufficiently persuaded of progress in that arena to mention fusion power as a possible game player. No dice?

Nuclear addressed above

Permalink Submitted by Dallas Kachan on Sun, 12/11/2011 - 15:33.

We talk about the possible impact of nuclear power in 2012 above in the section titled "storage investment to retreat." The 6 months of research we did this year for our latest new report on forthcoming nuclear innovations (the one you saw referenced in a blog, report info here) suggested renewable power storage could soon get a lot less important if these and other clean baseload power innovations are as disruptive as they appear to be.

Another forthcoming market change to be mention

Permalink Submitted by Frank Gagnon, W... (not verified) on Sun, 12/11/2011 - 11:37.

Thank you for this resume of the forthcoming market of venture capital for greentech. I like to add another point:

Presently the renewable energy depend on subsidies (feed in tariff is subsidy), and this increase investment risk with two factors:

- The market may vary drastically with government change, turning a profitable venture into nightmare over a day.

- The probable avenue of competitive technology that will be profitable without subsidies will make less efficient one obsolete.

This instability will disappear with new technologies that will not need subsidies to be sold and operated. At this point, VC investment will be increasing in volume, but decreasing in number.